Carbon removal is seen as a critical component in any climate mitigation strategy. The question markets are still answering is, what exactly will this look like in reality?

Dendra addresses the three primary areas of 1) compliance, 2) quality, and 3) management, and here we will be looking most closely at number 1, the foundations for meeting the needs of the compliance market.

The basic arithmetic of climate science requires arresting the advance of, and then reducing, greenhouse gas concentrations in the atmosphere. The primary levers to do so are:

The basic arithmetic of climate science requires arresting the advance of, and then reducing, greenhouse gas concentrations in the atmosphere. The primary levers to do so are:

- Emissions reduction: to decrease greenhouse gas release in the first place (eg through the adoption of renewables which would displace fossil-fuel electricity generation).

- Carbon removal: to capture, sequester or draw down those gases already in the atmosphere.

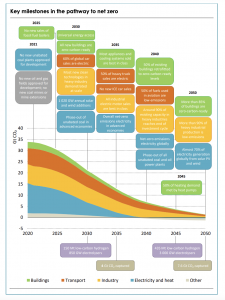

Much of the focus has been on reducing emissions, and for good reason. About 80% of the required decrease in net emissions by 2050 is forecast to come from cutting emissions. But there is broad agreement that there is a level of greenhouse gas emissions that will still be inevitable, and that existing and future greenhouse gases in the atmosphere will need to be removed.

Figure 1: Net Zero by 2050 (IEA, 2021).

To hit the net-zero threshold by 2050, or hopefully before, we will need to establish scalable ways to draw down those hard-to-eliminate emissions. This is why an increasing share of climate mitigation efforts and associated investments are now centred around how to best build a global carbon removal market.

The carbon removal market can be split into 2 primary categories:

- Technical: ‘Negative Emissions Technologies’ (NETs) which includes carbon capture and storage technologies (CCS).

- Environmental: ‘Nature-Based Solutions’ (NBS) which includes natural climate solutions (NCS) such as afforestation, reforestation and avoided deforestation.

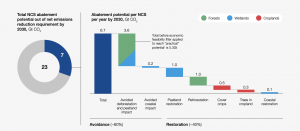

Figure 2: Natural carbon solutions (NCS) annual carbon sequestration potential (6.7 GtCO2e p.a.) through avoidance (blue; primarily conservation-focused, representing 55% of potential) and restoration (green; 45% of potential) activities (McKinsey Nature Analytics, 2021).

The climate and financial returns of a successful carbon removal market are large. For NCS alone, estimates vary in the range of 3 – 7 billion tonnes / year of carbon dioxide equivalent (CO2e), i.e. 3-7 Gt CO2e, which is certainly in the practically realisable range (McKinsey Nature Analytics, 2021). The price at which most nature-based sequestration projects become viable is US$30/ tCO2e, which would represent at least a US$90bn global market. In Australia alone, at the current compliance market price, it could become a US$120bn market and in the EU, where the current compliance market price is at €80 (US$86) (Sandbag, April 2022), this would represent a fully priced market of US$330bn. And this would be for carbon removal-generated credits alone i.e. excluding any priced emissions reduction market.

At Dendra, we specialise in nature-based solutions, specifically, natural climate solutions. Dendra focuses on restoration and reforestation, the activities that represent 45% of the overall NCS potential (shown in green in Figure 2). The primary activities contributing to NCS carbon removal include improvements to the sustainable management of:

- Agriculture

- Forestry & land use

across croplands, wetlands and forests, including activities such as reforestation, afforestation, and coastal and peatland restoration.

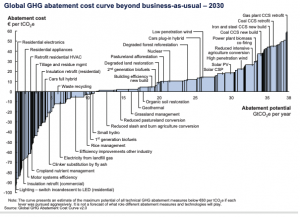

In order to understand the proposed rollout of these new technologies and methodologies, various carbon abatement cost curves have been proposed. These essentially provide a cost and quantity reflection of the potential carbon offsets generated by methodology, which is ultimately a supply curve for carbon offsets.

Figure 3: Example carbon cost abatement curve (McKinsey, 2009).

These curves imply sequencing; each carbon offset methodology would be adopted sequentially, from left to right, lowest cost to highest if adoption was purely based on cost and quantity. If this were the case, the majority of potential NBS-generated carbon offset projects would be financed as a cheap source of carbon offsets before moving on to CCS projects, which are typically more expensive.

However, to realise the full potential of carbon removal through each of these methods, it’s not just meeting the base compliance needs, high quality in all carbon removal activities is a must. It is essential that projects satisfy the Kyoto Protocol requirements of additionality, measurability and permanence. This is crucial not just for robust financial returns, it’s also to ensure that the environmental challenge can be tackled in a timely and effective way.